Disclosure to action

CSRD and science-based targets for nature

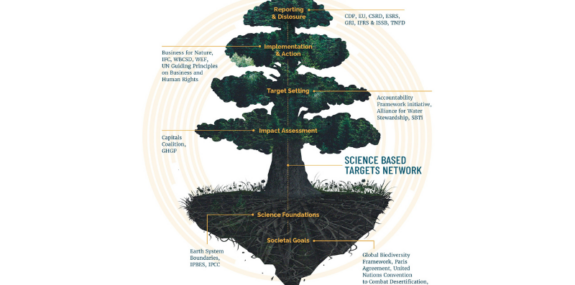

At a glance

This introduction to the EU’s Corporate Sustainability Reporting Directive (CSRD) and science-based targets (SBTs) for nature provides an overview of how they can work together to support companies in achieving their sustainability goals.

Complementing CSRD, SBTN empowers companies to actively address their impacts and quantify their contributions to nature-positive outcomes.

- Inform disclosures: Science-based targets for nature offer a rigorous and prescriptive approach (e.g., to materiality assessments) that generates data and insights that can inform companies’ CSRD disclosures.

- Beyond disclosures: While CSRD is focused on disclosure of impacts, SBTN goes a step further by providing a clear, science-based framework that empowers companies to actively address their impacts, showing how much action to take, where, and when, based on what nature needs.

- Long-term value: Setting science-based targets for nature helps companies build the capacity and resilience needed to adapt to emerging trends and stay ahead of future regulatory requirements, creating enduring value for the business.

We are grateful to the following subject matter experts for their contributions: Sam Sinclair and Peter McCann from Biodiversify, Carly Sibilia and Beatrice Boarolo from ERM, Stefan Jimenez from Deloitte & Touche LLP, and Guillaume Wahl and Christopher Rannou from WWF.

Introduction to CSRD

The EU’s Corporate Sustainability Reporting Directive (CSRD) requires companies to disclose information on their impact, risks, and opportunities concerning environmental, social, and governance (ESG) issues. Beatrice Boarolo (ERM), explains the significance of the CSRD:

“The CSRD represents a significant advancement of corporate sustainability reporting, setting a new standard for corporate transparency and accountability on ESG topics. The ambition is to provide standardized, consistent, and reliable sustainability reporting with respect to existing regulatory frameworks worldwide.”

While the disclosure requirements of CSRD are outlined in the European Sustainability Reporting Standards (ESRS), in this piece we will refer to the CSRD throughout for consistency and to avoid confusion.

SBTs and CSRD: complementary yet distinct

Science-based targets (SBTs) for nature equip companies to address their environmental impacts by taking measurable, place-based action, based on ecological and social thresholds.₁ They are developed by the Science Based Targets Network (SBTN), a voluntary civil society-led initiative.

Both CSRD and SBTs for nature can support transitions to more sustainable corporate practices. They are complementary yet distinct, aiming to achieve different outcomes:

- Type: SBTs for nature are developed by SBTN, a voluntary, civil society-led initiative while CSRD is mandatory EU legislation, although it has some voluntary components.

- Purpose: CSRD is designed to increase corporate transparency and provide decision-useful information to stakeholders through disclosures; it does not prescribe sustainability actions or performance beyond disclosures.₂ SBTN’s methods are focused on assessing and addressing impacts through setting science-based targets, and are prescriptive about which targets are set and how this is done.

- Scope: SBTs for nature are aimed at corporate end users across the world,₃ while CSRD is aimed at companies based or with significant operations in the EU. CSRD also encompasses a broader set of environment, social, and governance topics than SBTN’s methods, and more fully accounts for the downstream value chain.₄₅

- Focus: CSRD and SBTs for nature both support a double materiality approach. CSRD requires disclosures based on impact and financial materiality, including a company’s material dependencies on nature. Financial materiality and dependencies are both considered in SBTN’s methods in the prioritization step (Step 2C), although the explicit focus of the methods is on impact materiality.

This introductory piece outlines the ways in which CSRD and science-based targets for nature can be considered complementary.

We explore this through three possible use cases for setting SBTs for nature in the context of CSRD:

- Inform disclosures

- Beyond disclosures

- Long-term value

While setting SBTs for nature can help companies meet their CSRD requirements to a high degree, it does not guarantee compliance, as CSRD is broader and necessarily has specific requirements.

“CSRD is not prescriptive about the methodologies or tools that should be used. SBTN brings clarity by providing these.” Christopher Rannou

WWF

1. Inform disclosures

Science-based targets for nature offer a rigorous and prescriptive approach that generates data and insights that can inform companies’ CSRD disclosures.

For example, CSRD requires that companies conduct a materiality assessment, but does not prescribe how it should be undertaken.₆ Therefore, it is up to companies to decide on the approach they take to conduct their materiality assessment, which could have a significant impact on what is included in the disclosures.

While this flexibility may be welcome for some companies, for others it could leave them with concerns about whether their stakeholders will approve of their methods. WWF explain this clearly in their Corporate Nature Targets report:

“While some guidance on methodology is given (notably by recommending the use of initiatives like TNFD or SBTN), it’s crucial to understand that the main emphasis of the CSRD is on the disclosure of these elements (or a rationale for their omission if the entity deems them not material), rather than on the quality of the information provided (i.e. corporate practices).”₇

“Using an independent set of methods shows that you haven’t just cherry-picked the methods.” Peter McCann

Biodiversify

SBTN’s methods are prescriptive, requiring companies to assess and prioritize their impacts, with clear thresholds for materiality and accounting for state of nature variables. Christopher Rannou (WWF) is clear on the usefulness of SBTs for nature for the companies they work with:

“Many companies do not know how to generate some insights needed to inform their disclosure requirements because CSRD is not prescriptive about the methodologies or tools that should be used. SBTN brings clarity by providing these.”

Peter McCann (Biodiversify) echoes this, explaining the benefits of taking a rigorous approach:

“If you use SBTN methods as a basis for parts of CSRD, your methods will stand up to stakeholder scrutiny. Using an independent set of methods shows that you haven’t just cherry-picked the methods.”

Additionally, SBTN is referenced in CSRD (ESRS E2-3, E3-3, and E5-3) as a source of guidance for companies to set targets, including where this involves considerations of environmental thresholds. The SBTN methods provide clear guidance on how these thresholds can be established and how responsibility for them can be allocated.

Companies disclosing through CSRD have also found value in following the SBTN methods when sourcing state of nature variables (Step 1B), prioritizing impacts (Step 2), and conducting stakeholder consultations (see Stakeholder Engagement Guidance). Companies have reported using SBTN tools such as the materiality screening tool and High Impact Commodity List (HICL) to inform their CSRD reporting. Broad uptake of SBTN methods would help ensure consistency in approaches to assessing impacts, which would assist with improving comparability between companies.

Carrefour attest to the complementarity of science-based targets with CSRD:

“By applying the SBTN approach, we are more prepared to meet the requirements of the CSRD, thanks to a highly thorough method.”

This will only increase over time as SBTN expands methods and guidance, for example on ocean targets, enablers, taking action (Step 4), and validating results (Step 5).

2. Beyond disclosures

While CSRD is focused on disclosure of impacts, SBTN goes a step further by providing a clear, science-based framework that empowers companies to actively address their impacts, showing how much action to take, where, and when, based on what nature needs.

Peter McCann (Biodiversify) explains why taking an integrated approach to taking action beyond disclosures matters:

“If you do the bare minimum for CSRD, you might meet the regulatory requirements but you may not be able to use it to inform business decisions. For a rigorous analysis that can inform business decisions, set science-based targets for nature.”

WWF considers that “nature targets are essential to set the ambition for entities’ nature transition planning”, and that SBTN’s methods “represent the gold standard framework for setting nature targets”. This perspective on SBTs for nature is shared by the companies that have piloted them, with one reporting:

“We believe in the power of the output and that is what makes it worth embarking on the journey… SBTN’s assessment helped in conversations about capital allocation and procurement, and there is benefit in that.”

“For a rigorous analysis that can inform business decisions, set science-based targets for nature.” Peter McCann

Biodiversify

For example, companies piloting SBTs for nature have uncovered hidden risks within their value chains, prompting them to take action where it really matters. As one SBTN pilot company attests:

“After getting the Steps 1 & 2 results, we took quick actions to mitigate risk for some sourcing locations”.

Going beyond disclosures is also important in proving to investors and other stakeholders that the company is committed to addressing its impacts and risks. With CSRD, even where it is optional whether companies, for example, set targets for different impacts, they have to explain clearly why they have chosen not to do so. As Carly Sibilia (ERM) explains:

“With CSRD, it’s clear when companies have done the bare minimum, especially where their assessment of nature-related impacts is disconnected from the ecological context.”

For example, in the CSRD (ESRS E2), a company must disclose whether it has set pollution targets, and if so what these are, but it does not need to have actually set them. Where it has set targets, it is optional whether the company takes ecological thresholds into account. Investors and other stakeholders are able to see this, and may question the usefulness of any targets that have not taken ecological thresholds into account. So while CSRD does not require that targets are set, it points to best practice: setting science-based targets for nature that use ecological thresholds.

“With CSRD, it’s clear when companies have done the bare minimum.” Carly Sibilia

ERM

For Sam Sinclair (Biodiversify), companies will have to go beyond the bare minimum eventually:

“Standards and frameworks such as CSRD and TNFD are like nesting dolls because sooner or later you have to get to grips with the impacts of your supply chain, and SBTN is trying to do this in earnest.”

3. Long-term value

In the context of an increasingly ambitious regulatory landscape exemplified by CSRD, setting science-based targets for nature helps companies build the capacity and resilience needed to adapt to emerging trends and stay ahead of future requirements, creating enduring value for the business.

Stefan Jimenez (Deloitte & Touche LLP) emphasizes the significance of CSRD for companies’ need to stay ahead of regulations:

“CSRD represents a leap in sustainability regulation, intending to drive strategic and organization-wide change. It is important for companies to stay ahead of the curve.”

“By aligning to SBTN’s prescriptive approach, corporates are better able to anticipate regulatory requests.” Beatrice Boarolo

ERM

CSRD may anticipate similar regulations in other jurisdictions, and even where this does not happen, it may shift stakeholders’ expectations on sustainability reporting. Following SBTN’s methods provides a clear means for companies to pre-empt future requirements and expectations by engaging with more exacting requirements now. Beatrice Boarolo (ERM) explains:

“CSRD requirements will be expanded in the coming years with sectoral, non-EU, and SME standards in development, and some requirements are phased-in. By aligning to SBTN’s prescriptive approach, corporates are better able to anticipate regulatory requests, and improve their resilience against nature-related transition risks.”

Setting SBTs for nature provides other long-term benefits to companies, such as building institutional knowledge and capacity in nature, securing internal buy-in and funding, and developing impactful relationships with stakeholders (see our case studies for more on this).

Companies benefit from being part of the SBTN Corporate Engagement Program, and use this as an opportunity to learn more about how other companies are approaching emerging challenges, and to explore areas for collaboration. Setting targets can also help secure a reputational boost for those companies that decide to take early and decisive action on nature.

“[SBTN] is often seen as an endpoint or a box to tick, whereas in reality it is a powerful tool for informing business decisions.” Sam Sinclair

Biodiversify

For some, this might represent a different way of conceptualizing science-based targets for nature, as Sam Sinclair (Biodiversify) elaborates:

“There are lots of misconceptions about science-based targets for nature – it is often seen as an endpoint or a box to tick, whereas in reality it is a powerful tool for informing business decisions, building capacity, and generating value – it is a means to an end.”

This is a point echoed by Stefan Jimenez (Deloitte & Touche LLP):

“Science-based targets for nature should be seen as a potential way to create value through evidence-based planning and action, rather than merely complying with a voluntary standard.”

Further reading

This piece has been an introduction to SBTN and CSRD complementarity, so we have not included an exhaustive mapping of all of the different possible data overlaps between them. For further information on these overlaps, see WWF’s report “Corporates Nature Targets: Ensuring the Credibility of EU-Regulated Commitments”, available here; and Appendix 1 of their “Integrating companies within planetary boundaries” report, available here.

SBTN has also completed a high-level mapping of its connections with other sustainability initiatives, which can be found in Appendix 2 of the Step 1 Technical Guidance.

Carly Sibilia from ERM provides an overview of SBTN and CSRD alignment in this clip. For further information on global ESG regulations that have impacts on companies, see ERM’s ERM’s Global Regulations Radar.

Deloitte has produced an FAQs webpage on the CSRD, and a report entitled “Putting nature and biodiversity loss on the business agenda”.

The ESRS Commission Delegated Regulation can be found here. Further information on EFRAG’s ESRS workstreams is available here.